Managing the financial aspects of your small business can be a daunting task, especially when it comes to bookkeeping. However, with the right organization and tools in place, you can streamline this process and ensure the financial health of your enterprise. we’ll share practical tips to streamline your process. From setting up a system to tracking expenses, we’ve got you covered. Simplify your bookkeeping tasks with these strategies!

What is Bookkeeping?

Bookkeeping is a methodical process of recording, organizing, and managing financial transactions for your business. It includes keeping track of income, expenses, assets, liabilities, and equity. In simpler terms, it’s about maintaining accurate financial records that reflect the true financial position of your company. By practising precise bookkeeping, you can ensure a clear understanding of your business’s financial health and keep a track record of all your financial activities.

Why Accurate bookkeeping for small businesses is important.

Accurate bookkeeping is vital for small businesses for several reasons:

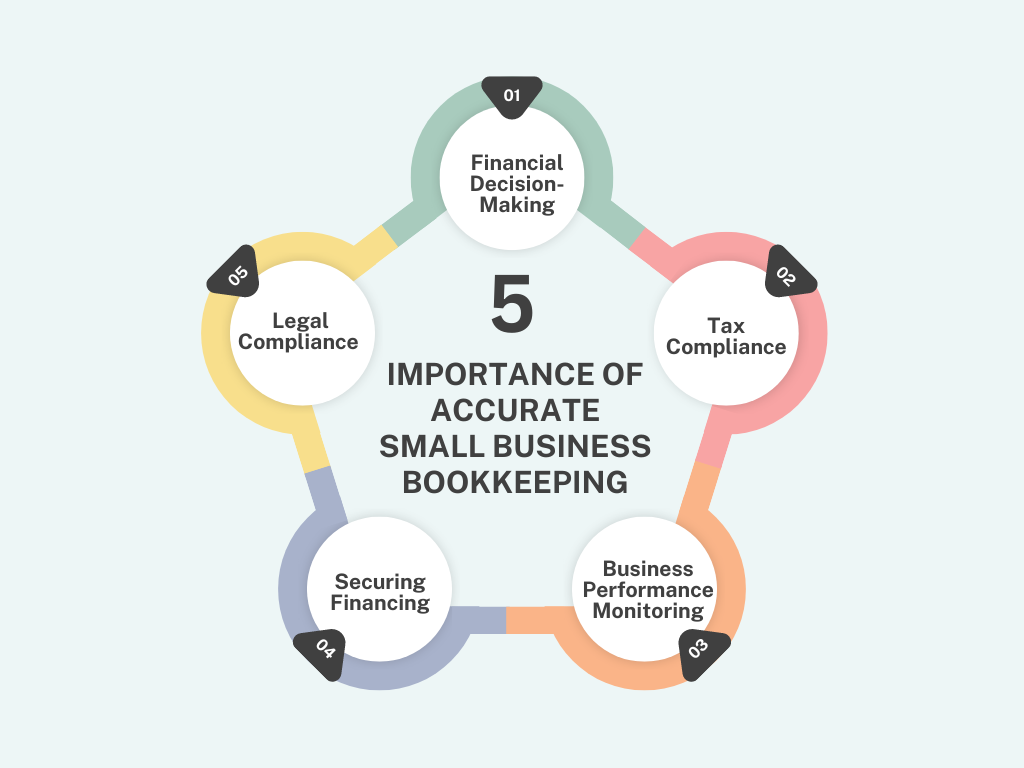

5 Importance of Accurate Small Business Bookkeeping

Financial Decision-Making: Accurate records provide the data you need to make informed financial decisions. Whether it’s deciding on investments, budget allocations, or pricing strategies, having reliable financial information is crucial for success.

Tax Compliance: Proper bookkeeping ensures you meet your tax obligations accurately and on time. It helps you track deductible expenses, claim eligible tax credits, and avoid penalties for non-compliance.

Business Performance Monitoring: By maintaining accurate records, you can monitor your business’s performance over time. Tracking key metrics such as revenue, expenses, and profitability allows you to identify trends, assess growth opportunities, and address any areas of concern.

Securing Financing: When seeking financing from banks or investors, accurate financial records are essential. Lenders and investors rely on these records to assess your business’s financial health and viability. Having well-organized books increases your credibility and enhances your chances of securing funding.

Legal Compliance: Proper bookkeeping ensures compliance with regulatory requirements and industry standards. It helps you avoid legal issues related to financial reporting, employee payroll, and tax filings. Non-compliance can result in fines, legal disputes, and reputational damage.

How to do bookkeeping for small businesses

When it comes to bookkeeping for small businesses, here are eight essential steps to follow:

Set Up a System: Start by choosing a bookkeeping system that works for you. Whether it’s using accounting software like QuickBooks, Zoho Books, MYOB, Xero, or a simple spreadsheet, find a method that suits your business’s needs and budget.

Choose an entry system. Before tackling small-business bookkeeping, consider single-entry and double-entry accounting systems. Your choice impacts financial management and record accuracy. For smaller, simpler businesses, single entry suffices, while larger or complex ones benefit from double entry. Consider business size, complexity, reporting needs, and long-term goals. Optimal selection sets the stage for effective financial management and informed decision-making.

Categorize your business transactions.

Assets: Resources owned by your business with economic value, like cash, inventory, and property, tracking your wealth and investments.

Liabilities: Debts and obligations owed to external parties, including loans and accounts payable, ensuring transparency and financial health assessment.

Equity: Ownership interest held by owners or shareholders, reflecting assets’ residual value after deducting liabilities, crucial for understanding ownership and business value.

Revenue: Income generated from primary business activities, such as sales, representing inflows of assets or decreases in liabilities, tracking performance and profitability.

Transfers: Movements of funds or assets between accounts within your business, essential for internal accounting, ensuring accurate recording and tracking of fund movements.

Track Income and Expenses: Record all sources of income, including sales revenue, interest, and investments. Similarly, track every business expense, from office supplies and rent to utility bills and employee wages. Categorize transactions accurately to facilitate reporting and analysis.

Maintain Organized Records: Keep all financial documents, such as receipts, invoices, and bank statements, organized and accessible. This makes it easier to reconcile accounts, prepare tax returns, and respond to any financial inquiries.

Reconcile Bank Statements: Regularly reconcile your bank and credit card statements with your accounting records to ensure accuracy. This involves matching transactions in your books with those on your statements and identifying any discrepancies.

Stay on Top of Tax Obligations: Familiarize yourself with your tax obligations, including filing deadlines and payment schedules. Set aside funds for taxes regularly to avoid cash flow issues when tax time rolls around. Consider consulting a tax professional for guidance on tax planning and compliance.

Review and Analyse Financial Reports: Regularly review your financial reports, such as profit and loss statements, balance sheets, and cash flow statements. These reports provide valuable insights into your business’s financial health and performance, helping you make informed decisions and identify areas for improvement.

Bookkeeping Tools and Software

Opting for online bookkeeping services can significantly streamline your financial management. These services offer user-friendly software like QuickBooks Online, Zoho Books, MYOB and Xero, providing features such as invoicing and expense tracking accessible from any device with an internet connection. With automation features, you can save time on repetitive tasks like data entry and reconciliation, reducing errors. Additionally, these platforms offer cloud-based storage for secure data backup and easy accessibility. Consider adopting these tools to enhance efficiency and focus on business growth.

Who should manage small-business bookkeeping tasks?

When it comes to managing small-business bookkeeping tasks, there are a few options to consider.

Owner or Entrepreneur: As the business owner, you have a vested interest in the financial health of your company. Managing bookkeeping tasks yourself allows you to have direct control over your finances and ensures that you stay informed about your business’s financial performance.

In-House Bookkeeper: Hiring an in-house bookkeeper can be beneficial if you have a high volume of transactions or complex financial needs. A dedicated bookkeeper can handle day-to-day bookkeeping tasks, such as recording transactions, reconciling accounts, and preparing financial reports, allowing you to focus on other aspects of running your business.

Outsourced Bookkeeping Services: If you prefer to focus on growing your business rather than managing bookkeeping tasks internally, outsourcing bookkeeping services is a viable option. Outsourced bookkeepers can provide expertise and efficiency, often at a lower cost than hiring an in-house bookkeeper. This option is particularly attractive for small businesses with limited resources or those looking to streamline their operations.

What are some of the challenges of small business bookkeeping?

Navigating small business bookkeeping comes with its fair share of challenges. Here are a few you might encounter:

Limited Resources: Small businesses often have limited financial resources, making it challenging to invest in sophisticated accounting software or hire dedicated bookkeeping staff. As a result, you may need to find cost-effective solutions that still meet your business’s needs.

Time Constraints: Running a small business involves wearing many hats, and bookkeeping can sometimes take a back seat to other priorities. Finding the time to stay on top of your financial records amidst the daily demands of managing your business can be a challenge.

Complexity of Transactions: Small businesses may deal with a variety of financial transactions, from sales and expenses to payroll and taxes. Keeping track of these transactions and ensuring they are accurately recorded can be daunting, especially as your business grows.

Regulatory Compliance: Staying compliant with tax laws and regulations can be challenging for small businesses, particularly if you’re not familiar with the intricacies of tax reporting. Failing to comply with regulations can result in penalties and legal issues down the line.

Data Security: Protecting sensitive financial data is essential for small businesses, but it can be challenging without the resources to invest in robust cybersecurity measures. Ensuring the security of your financial records and preventing data breaches requires vigilance and proactive measures.

Conclusion

As a business owner, it is crucial to understand your company’s financial health, as it serves as the foundation for informed decision-making. This understanding begins with having updated and accurate books, where every transaction is meticulously recorded and organized. Bookkeeping not only ensures compliance with regulatory requirements but also provides the essential data needed to make strategic decisions about hiring, marketing, and growth. By maintaining precise financial records, you can extract valuable insights into your business’s performance, identify areas for improvement, and capitalize on growth opportunities. Whether it’s assessing profitability, evaluating cash flow, or forecasting future financial needs, reliable bookkeeping lays the groundwork for sound business decisions.

FAQs

Q.1 What are the key elements of small business bookkeeping?

A: Key elements of small business bookkeeping include recording income from various sources, tracking expenses such as rent, utilities, and wages, managing accounts receivable and payable, reconciling accounts with bank statements, and generating financial reports like income statements, balance sheets, and cash flow statements.

Q.2 What are some effective strategies for organizing small business bookkeeping?

A: Use cloud-based accounting for streamlined records. Customize chart of accounts for accuracy. Set regular schedules for transactions and reports. Keep separate accounts for clarity. Record receipts for tax compliance. Review and adjust for efficiency.

Q.3 What kind of bookkeeping is used by small businesses?

A: Small businesses typically use either single-entry or double-entry bookkeeping. Single-entry is simpler, suitable for very small businesses, and involves recording transactions once. Double-entry is more comprehensive, widely used, and involves recording each transaction twice for accuracy and detailed financial insights.